GET A FREE PROTECTION REVIEW AND SEE IF YOU HAVE THE RIGHT LIFE INSURANCE!

How to Use POD and TOD Designations to Avoid Probate

Avoiding probate doesn’t have to be complicated or expensive. One of the easiest ways to ensure your money and property transfer smoothly to your loved ones is by setting up Payable on Death (POD) and Transfer on Death (TOD) designations. These simple tools let your bank accounts, investments, and even real estate pass directly to your beneficiaries—without lawyers, court delays, or unnecessary fees.

ALL POSTSLIFE INSURANCE

11/4/20253 min read

How to Use POD and TOD Designations to Avoid Probate

When it comes to protecting your loved ones and making sure your assets are transferred smoothly after you pass away, one of the simplest and most effective estate planning strategies is using POD (Payable on Death) and TOD (Transfer on Death) designations. These tools allow your money and investments to go directly to your chosen beneficiaries—without going through the lengthy and expensive probate process.

What Is Probate—and Why Avoid It?

Probate is the court-supervised process of settling a deceased person’s estate. It ensures debts are paid and assets are distributed according to the will (or state law, if there’s no will). While it serves a purpose, probate can take months—or even years—and often costs thousands in court fees, attorney expenses, and administrative costs.

Probate also makes your estate public record, meaning anyone can see what you owned and who received it. Most families prefer to avoid this for privacy and convenience.

The good news: POD and TOD designations let your assets transfer automatically to your beneficiaries, bypassing probate entirely.

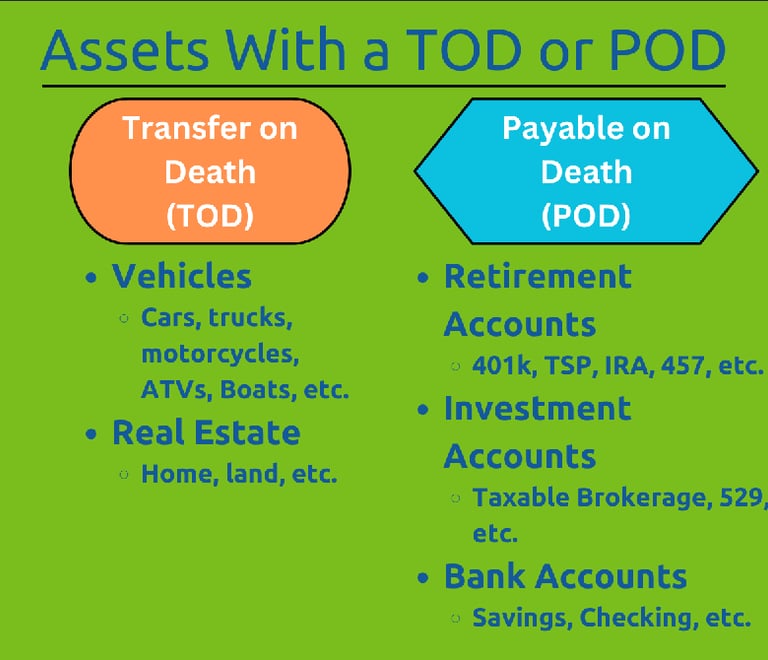

What Is a POD (Payable on Death) Account?

A Payable on Death (POD) designation applies primarily to bank accounts—checking, savings, money market, and certificates of deposit. When you set up a POD beneficiary, you’re naming someone who will inherit the funds in that account after you pass away.

Here’s how it works:

You remain the sole owner of the account during your lifetime.

Your beneficiary has no rights to the money while you’re alive.

Upon your death, your beneficiary simply presents a death certificate to the bank, and the funds are transferred directly to them—no probate required.

You can usually set up a POD designation by completing a simple form at your bank. It’s quick, free, and can save your heirs time, stress, and legal fees.

What Is a TOD (Transfer on Death) Designation?

A Transfer on Death (TOD) designation works similarly but applies to investment accounts and certain real estate titles. Brokerage firms, for example, let you register your stocks, bonds, or mutual funds with a TOD beneficiary. When you pass away, ownership of those assets transfers immediately to that person.

In some states, you can even use a TOD deed for real estate—allowing your home or property to pass directly to a beneficiary without going through probate. Like PODs, TOD designations don’t affect your ownership during your lifetime.

Setting up a TOD registration usually requires filling out a beneficiary form with your financial institution or recording a TOD deed with your county recorder’s office for real property.

Benefits of Using POD and TOD Designations

Avoids Probate: Your designated beneficiaries receive assets quickly and directly, often within weeks.

Saves Money: Avoiding probate can save thousands in legal and court fees.

Maintains Privacy: Transfers happen outside the public record.

Easy to Set Up: Usually requires only a short form with your bank or brokerage.

Retains Control: You can change or revoke the designation anytime during your lifetime.

Things to Watch Out For

While POD and TOD designations are powerful tools, they must be used carefully to avoid unintended problems.

Coordinate with your overall estate plan. If your will says one thing and your POD/TOD designations say another, the POD/TOD takes precedence. Always keep your beneficiary designations consistent with your will and trust.

Name contingent beneficiaries. If your primary beneficiary passes away before you and no alternate is named, the asset may still go through probate.

Consider special situations. If a beneficiary is a minor or has special needs, you may want to leave assets through a trust instead of directly through a POD or TOD.

Stay up to date. Review your designations after major life events like marriage, divorce, births, or deaths. Outdated beneficiaries are one of the most common estate planning mistakes.

How to Set Up POD and TOD Designations

Contact your bank or brokerage firm. Ask for a “Payable on Death” or “Transfer on Death” form.

Provide beneficiary details. Include full legal names, addresses, and Social Security numbers if possible.

Submit and keep records. Keep copies with your other estate planning documents and let your executor or family know where to find them.

Review annually. Life changes—make sure your designations still reflect your wishes.

If you own real estate, check whether your state allows Transfer on Death deeds (also called beneficiary deeds). Many states now do, and they can be a simple, low-cost way to keep your home out of probate.

The Bottom Line

POD and TOD designations are among the easiest ways to make sure your assets go where you want them to—without lawyers, courts, or unnecessary delays. While they don’t replace a full estate plan or will, they are a crucial piece of a smooth, cost-effective transfer strategy.

By taking just a few minutes to set them up, you can give your loved ones peace of mind and ensure your legacy is handled exactly as you intended.

If you want to make sure your accounts, insurance, and investments are properly set up to avoid probate and protect your family’s financial future, I can help.

📞 Contact Scott Reinhart today to schedule a complimentary review and learn how POD and TOD designations fit into your overall protection plan.

👉 Visit IntegrityAdvantageGroup.com/contact to get started and take the next step toward peace of mind.