GET A FREE PROTECTION REVIEW AND SEE IF YOU HAVE THE RIGHT LIFE INSURANCE!

Understanding Index Universal Life Insurance (IUL): How It Works and How to Keep It Healthy

Discover how Index Universal Life (IUL) insurance works, including its flexible death benefit, cash value growth, and living benefits. Learn practical tips to keep your policy healthy, ensure it stays fully funded, and make the most of this powerful financial tool for protection and wealth building.

LIFE INSURANCEALL POSTS

Created by Scott Reinhart

9/10/20254 min read

Understanding Index Universal Life Insurance (IUL): How It Works and How to Keep It Healthy

When most people think of life insurance, they picture a policy that pays out when they die. That’s true, but some policies—like Index Universal Life Insurance (IUL)—can do much more. An IUL not only provides lifelong coverage, but it also has a unique cash value component that grows over time. This combination makes it a powerful financial tool, but it also means you need to understand how it works to get the most out of it.

Let’s break it down in simple terms.

What is an IUL?

An Index Universal Life Insurance (IUL) policy is a type of permanent life insurance. Unlike term life, which only covers you for a set number of years, an IUL is designed to last your entire life—as long as you keep enough money in the policy to cover the monthly costs.

Think of it like owning a car. As long as you keep gas in the tank and take care of maintenance, the car will keep running. With an IUL, your “gas” comes from premium payments and the cash value growth inside the policy.

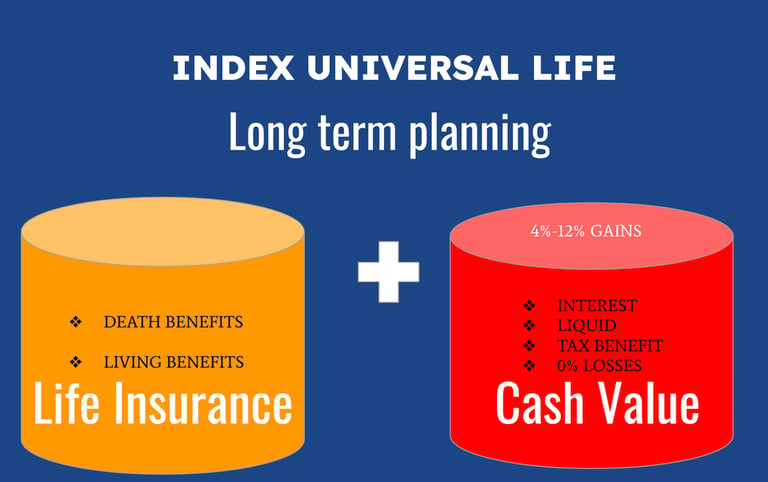

The Two Main Parts of an IUL

Death Benefit

This is the payout your loved ones receive when you pass away.

It’s designed to last for life, not just for a term of years.

Cash Value

This is money that grows inside your policy, based on how a stock market index (like the S&P 500) performs.

The good news is that your money isn’t directly invested in the market, so it won’t lose value when the market drops. Instead, it grows when the market goes up—up to a cap.

This cash value can be used while you’re alive, giving you a living benefit in addition to your death benefit.

What Are Living Benefits?

One of the most overlooked advantages of an IUL is the ability to use the policy while you’re still alive. These are called living benefits.

Here are the main ways they work:

Cash Value Access

You can borrow against the cash value in your policy—usually tax-free—without having to go through a bank. This can be used for retirement income, education costs, emergencies, or even opportunities like investing in a business.Chronic, Critical, and Terminal Illness Riders (if included)

Many IULs come with riders that let you access part of your death benefit early if you’re diagnosed with a serious illness or injury. For example:If you suffer a stroke, heart attack, or cancer diagnosis, you may be able to accelerate part of your death benefit.

If you become chronically ill and can’t perform certain daily activities, the policy can help cover care costs.

If you’re diagnosed as terminally ill, you can receive funds in advance to relieve financial stress.

Flexible Premiums

If times get tough, an IUL gives you flexibility. Instead of missing a payment and losing coverage (like term insurance), your policy’s cash value can step in to cover costs temporarily.

In short: living benefits mean your life insurance isn’t just for when you die—it can also protect you and your family during life’s toughest challenges.

How Long Does It Last?

You might have heard the phrase:

“Death benefit for life, as long as premium payments cover the monthly deductions.”

Here’s what that means:

Every month, the insurance company takes out a small deduction to pay for the cost of insurance and policy expenses.

As long as there’s enough money in the policy to cover those deductions—either from your premium payments or the cash value you’ve built up—the policy stays active.

If the account ever runs too low, the policy could lapse, meaning you’d lose coverage.

How to Keep an IUL Healthy

Here are the three keys to making sure your IUL works for you long-term:

1. Pay Consistently

Always make your premium payments on time. If possible, pay more than the minimum. This builds up your cash value faster and provides a cushion for years when interest credits are lower.

2. Review Annually

IULs are flexible, which is great—but it also means you need to check in. Every year, review your policy with your agent. Look at how your cash value is performing and whether adjustments are needed. Sometimes you may need to increase your payments to keep things on track.

3. Manage Loans Wisely

One of the best features of an IUL is the ability to borrow against the cash value, often tax-free. This can be a smart way to access money for emergencies, retirement, or big expenses. But be careful:

If you take a loan, make sure to pay back what you can.

At the very least, cover the interest so it doesn’t eat away at your cash value.

If loans aren’t managed properly, they can cause your policy to shrink—or even collapse.

Why Choose an IUL?

Many people like IULs because they offer:

Lifelong coverage (unlike term life, which eventually ends).

Cash value growth that’s tied to the stock market without the downside risk.

Living benefits that can be used during your lifetime.

Flexibility in premiums and benefits.

Options for tax-advantaged income in retirement

Compared to whole life insurance, an IUL is usually more affordable, with more growth potential. Compared to term life, it provides coverage for your entire lifetime, not just 10, 20, or 30 years.

The Bottom Line

An Index Universal Life Insurance policy can be one of the most powerful financial tools you own—but only if you understand how it works. The key is to keep it funded, review it regularly, and be smart about loans. Do that, and your IUL can give you both protection and peace of mind for life.

With the added advantage of living benefits, you don’t have to wait until you pass away for your policy to matter. It can provide security, flexibility, and financial relief for you and your loved ones throughout your life.

Stay funded. Stay covered. Stay secure.